PF Withdrawal – Employees’ retirement savings are held in PF, or provident fund. In other words, after retirement, money is given to employees who made PF contributions while they were employed. EPF contributions cannot be withdrawn by employees until they are retired. The sum can be withdrawn in certain circumstances where this rule does not apply. Read below to get detailed information related to PF Withdrawal like highlights, Revision of Rules, New Rules, Types, Necessary Documents, Steps for EPF Withdrawal Online, and much more

PF Withdrawal Online 2024

Employees’ Provident Fund (EPF), often known as PF (Provident Fund), is a required retirement savings plan for workers at qualifying organizations. After retirement, the corpus of this fund will be available to the employees. Employees are required to contribute 12% of their base pay to this fund each month under EPF regulations. To the employee’s PF account, the company makes a matching contribution. Every year, interest is earned on the funds put in EPF accounts. When an employee retires, they can withdraw their whole EPF balance.

EPF Withdrawal Details in Highlights

| Name | PF Withdrawal |

| Full Form | Provident Fund Withdrawal |

| Beneficiaries | Employees |

| Official Website | https://www.epfindia.gov.in/site_en/index.php |

Revision of Rules for Provident Fund Withdrawal

A number of the rules concerning withdrawals from the Provident Fund (PF) account have been updated by the Employees’ Provident Fund Organization (EPFO) for 2024. These changes are intended to make it simpler for subscribers who are struggling financially as a result of the coronavirus outbreak to access their PF money. The new regulations provide that holders of PF accounts may withdraw up to 75% of their net PF or EPF account balance, or an amount equal to three months’ worth of their basic pay + dearness allowance, whichever is less. We’ll consider this to be a non-refundable deposit. You can file these withdrawal claims online. While offline claims can take up to 20 days to be resolved, online claims are required to be resolved in 3 working days.

PF Withdrawal New Rules

- The money in your EPF profile cannot be withdrawn while you are employed, much like in a savings account. The EPF is a comprehensive retirement savings program. The money cannot be reclaimed until after retirement.

- In the event of a catastrophe, such as a medical emergency, the purchase or construction of a home, or the pursuit of higher education, partial withdrawals from EPF funds are permitted. There are limitations to partial removal depending on the cause. A partial transfer request can be made online by the account owner.

- The EPF capital may be reclaimed if a person loses their job due to a deadbolt or layoff.

- The member of the EPF must file for bankruptcy to get the EPF payout.

- Retirement plans are not recognized until the person reaches a particular age, which is fifty-five, even though the EPF money may only be withdrawn after retiring. If the person is at least 54 years old, EPFO permits a drawdown of 90 percentage points of the EPF capital one year before retirement.

- The new rule states that after one month of being jobless, EPFO permits withdrawals of up to 75% of your EPF capital. The remaining 25% of the total capital can be changed to a different EPF profile after finding new employment.

- It used to be possible to withdraw your entire EPF amount after two months of being jobless.

- Only if a worker contributes to their EPF profile for 5 consecutive years is tax exemption on the EPF fund available. The worker’s EPF balance is taxed if there is a gap in contributions to the portfolio for five years in a row. The entire EPF amount will thereafter be considered a tax liability for the fiscal year.

- Taxes are withheld at the source whenever an EPF corpus is prematurely withdrawn. If the overall amount is less than Rs. 50,000, TDS is not applied. If an employee submits PAN along with the request, the applicable TDS amount is 10 percentage points. Alternatively, the price will be 30% plus taxes. A user’s entire revenues are not charged, according to the statement document 15H/15G, and the TDS can therefore be avoided.

- Workers no longer need to remain to wait for their boss’ approval before receiving their EPF payments. If the individual’s Aadhaar and UAN are connected and the firm has approved it, it is feasible to do it right away through the EPFO. Online verification of an EPF transfer’s status is possible.

Provident Fund Withdrawal Types

There are three types of PF redemptions available to participants who have joined EPFO and linked their Aadhar card information to their UAN:

- PF Final Agreement: When a person reaches retirement age and subsequently loses their work, the PF Final Agreement is released

- PF Partially Withdrawn: A transfer performed in the event of a tragedy

- Withdrawal of Pension Benefits

PF Withdrawal before Five Years of Service

TDS is applied to EPF withdrawals made before five years of continuous service. However, no TDS is taken from a withdrawal that is less than Rs. 50,000. The following EPF withdrawal guidelines should be kept in mind if you choose to withdraw your funds before five years of service:

- The assessee must annually submit a thorough breakdown of the whole amount deposited in PF accounts, per the most recent changes to ITR Forms 2 and 3.

- This will make it easier for the Income Tax Department to determine whether or not the withdrawal you made is taxable.

- The agency will also determine whether you need to pay any additional taxes following the revaluation.

- Employee, employer, and interest on each deposit are the four components of the EPF contribution.

- All four components will be taxed if the employee previously sought exemption from EPF contributions under Section 80-C.

- At the time of withdrawal, the employee’s contribution portion will be tax-free if they have not already requested an exemption from EPF.

- The tax will be determined by the employee’s income bracket for that particular year.

- Although the consideration will be made for each year, the tax will be applicable in the year of withdrawal.

EPF Withdrawal after Retirement

- According to the EPF Act, a member must submit a claim for his final compensation when he or she retires at age 58.

- The combined PF balance is made up of both employee and employer contributions.

- If the member has served for more than 10 years in continuation, he or she also qualifies for the EPS amount.

- The member may take his entire EPS amount combined with his EPF if he has not yet served for 10 years at the time of retirement.

- The employee receives pension benefits following retirement if he completes 10 years of service.

- At retirement, the EPF account’s corpus can be withdrawn entirely tax-free.

- Following retirement, the interest accumulated on the EPF corpus is taxable.

- Employees who have enrolled for EPF membership can fill out the form and submit their claims online.

- Following retirement, the member must pay tax on interest earned if he does not take money for three years.

Necessary Documents for Provident Fund Withdrawal

Some of the important documents required for PF Withdrawal are as follows:

- The employer can provide the UAN (Universal Account Number), which is a necessary condition.

- The name as it appears on the EPF account must accompany the bank account information in writing.

- The provident fund holder must have a bank account since money cannot be transferred to a third party while the holder is still alive.

- The identity evidence and personal details, such as the father’s name and birthdate, should match exactly.

- When an employee leaves the company, the employer must notify EPFO (Employee Provident Fund Organization) of the details. Both the joining and departing dates must be specified in detail.

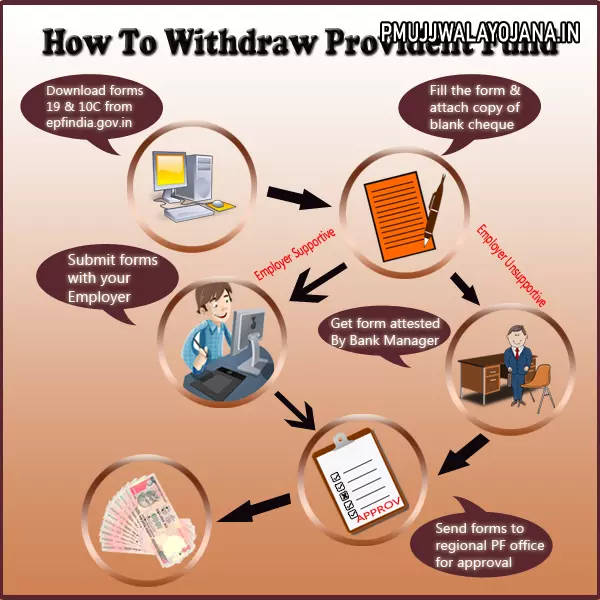

Step by Step Process for PF Withdrawal Online

By following the steps listed below, employees can submit a request for a PF withdrawal on the EPFO member portal.

- First of all, go to the official website of the Employees’ Provident Fund Organization (EPFO) Portal

- The homepage of the website will open on the screen

- Click on the Services tab followed by For Employees

- A new page will open on the screen

- Now, under the services tab, click on the Member UAN/Online Service (OCS/OTCP) option

- A new page will open on the screen

- Now, enter your UAN, password, and Captcha code to get logged in to your registered account

- Once you are successfully logged in, click on the KYC option under the Manage tab

- A new page will open on the screen

- Scroll down the page to the Digitally Approved KYC section

- Now, check all your KYC details and make sure that all the details are correct

- If all of the KYC information is accurate, select the Online Service link from the top menu to proceed with the withdrawal.

- Click on the CLAIM (FORM-31, 19 & 10C) option

- ONLINE CLAIM (FORM 31, 19 & 10C) form will open on the screen

- Now, enter the Last 4 digits of your registered bank account number and also verify it

- After successful verification of the bank account, a Certificate of Undertaking will be generated

- Finally, click on the Proceed for Online Claim option

- Now, for online fund withdrawal, click on the PF ADVANCE (FORM – 31) option

- From the drop-down menu next to the “Reason for which advance is required” option, choose a reason for the claim. It is also necessary to fill out the sections for the employee’s address and the advance amount.

- Now, click on the checkbox and submit your withdrawal application

- After that, upload the required documents that depend on the nature of the withdrawal

- The withdrawal amount will be taken from the EPF account and deposited to the appropriate bank account if the employer accepts the withdrawal request. You will get an SMS notice on your registered cellphone number once the claim has been resolved.

PF Withdrawal Taxation

- TDS is taken off of withdrawals made before five years of service have passed.

- When a withdrawal is made, TDS is taken out at a rate of 10% if a PAN is provided and 34.608% if one is not.

- However, no TDS is taken out of a withdrawal that is less than Rs. 50,000.

- TDS, however, is not applicable in several of the following situations.

- When a service is terminated due to circumstances beyond your control, the TDS rule does not apply. The possibility of company lockouts, retrenchments, staff layoffs, etc.

- When the service cannot be continued owing to a serious medical condition such as a physical handicap or mental disability, TDS is not applicable.